The 1/3 Rule for Financial Stability: Balance Your Income, Savings & Expenses the Smart Way

Nikita Roy

26, January, 2026 1 min read

The 1/3 Rule for Financial Stability: Balance Your Income, Savings & Expenses the Smart Way is the emerging gold standard for sustainable wealth building in 2026. It reflects a growing realization across households and economies that stability no longer comes from rigid formulas, but from proportional discipline—allocating income with intention while preserving flexibility in an unpredictable financial climate.

Executive Definition

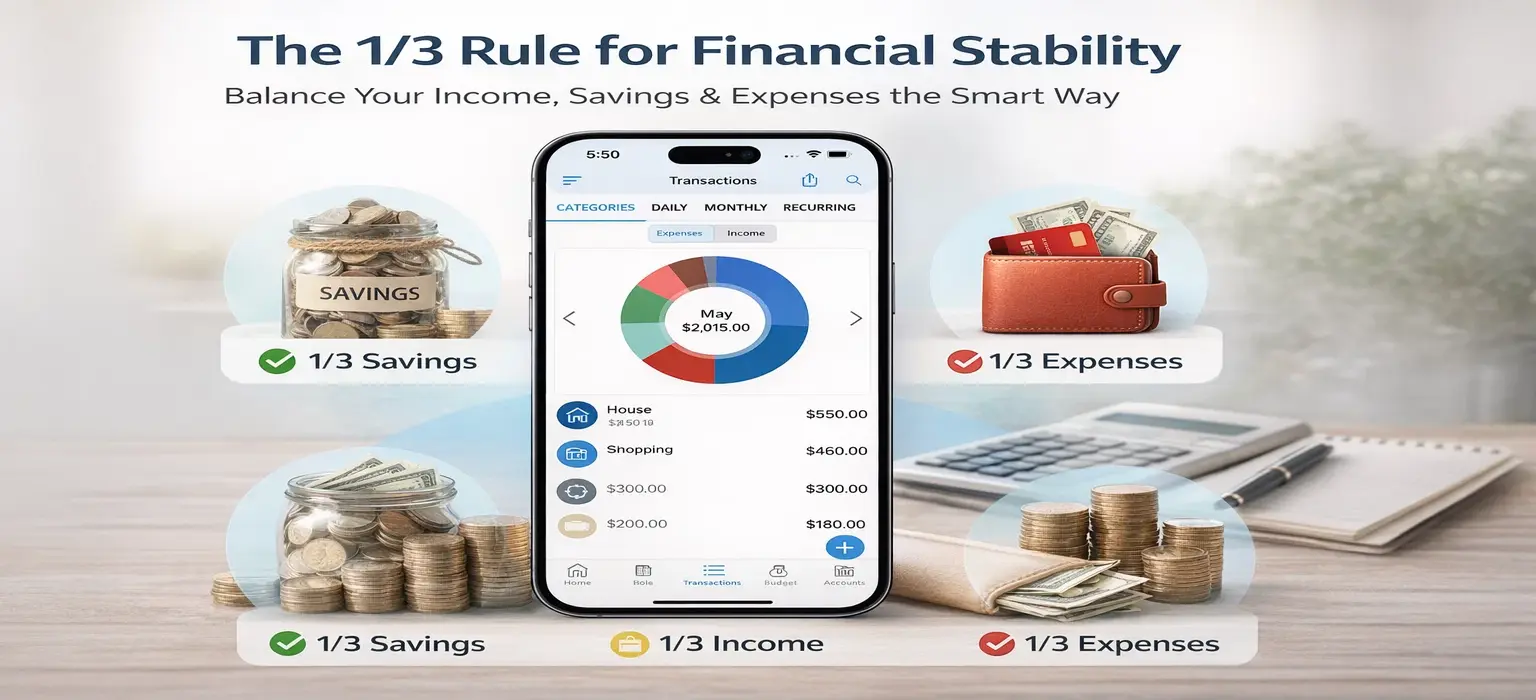

The 1/3 Rule for financial stability is a proportional budgeting framework that divides net income into three equal parts: one-third for essential living expenses, one-third for savings and long-term wealth building, and one-third for discretionary spending. It emphasizes balance, resilience, and adaptability in high-inflation, high-volatility economies.

We are living through a structural shift in personal finance. Inflation cycles are shorter, income streams are more fragmented, and financial stress is increasingly tied to cognitive overload rather than pure scarcity. In this environment, our goal is not optimization at all costs—it is equilibrium. The 1/3 Rule offers exactly that: a system that scales across income levels, geographies, and life stages while remaining psychologically sustainable.

The Mathematics of Peace: Deconstructing the 1/3 Rule for Global Markets

At its core, the 1/3 Rule is an exercise in capital allocation. Instead of chasing perfection, it enforces proportional boundaries that protect against extreme outcomes. Traditional models assume predictable expenses and steady growth. Global markets in 2026 do not cooperate with those assumptions.

Whether we are navigating the rental markets of Sydney, the tech hubs of Bangalore, or the financial districts of Zurich, the underlying tension is the same: fixed costs are rising faster than wages, and discretionary spending is increasingly invisible. Proportional budgeting restores fiscal granularity—the ability to see where each unit of income truly belongs.

Modern wealth management starts with a robust budgeting app that can model these proportions dynamically rather than locking users into static categories. This is why TimelyBills positions budgeting as a living system rather than a monthly spreadsheet: Budgeting App

Allocating for Survival: Why One-Third of Your Income Belongs to Living Essentials

The first third is non-negotiable. Housing, utilities, food, insurance, transportation—these are the foundations of economic survival. Capping essentials at roughly 33% of net income forces structural decisions early, before lifestyle inflation hardens into obligation.

This boundary is not about deprivation. It is about debt-to-income equilibrium. When essentials creep beyond one-third, every other financial function degrades: savings stall, stress rises, and discretionary spending becomes compensatory rather than intentional.

Leveraging a Bill Organizer to Automate Essential Outflows

The administrative burden of the “Expenses” third is solved by a dedicated bill organizer that ensures essentials are paid on time, without mental overhead. Automation here is not convenience—it is risk mitigation. TimelyBills removes late fees, missed renewals, and attention drain by centralizing obligations into a single system: Bill Organizer

Peace of mind is often just operational excellence applied consistently.

The Growth Quotient: Securing Your Future with One-Third Savings

The second third is where long-term stability is built. Saving 33% reframes wealth accumulation as a default behavior rather than an aspirational one. This portion supports emergency funds, investments, education, and future optionality.

Unlike percentage-light models, the 1/3 Rule treats savings as equal in importance to survival. This is a subtle but powerful psychological shift. We stop asking whether we can afford to save and start asking whether we can afford not to.

Scaling Ambition with a Goal Tracker for 2026 and Beyond

Visualizing your “Savings” third growth requires a high-resolution goal tracker that translates abstract intent into measurable progress. Goals anchored to time horizons and cash flow adapt as life changes. TimelyBills enables this transition from passive saving to active achievement: Goal Tracker

Growth accelerates when progress is visible.

Managing the Remaining Third: Discretionary Spending without Guilt

The final third is often misunderstood. This is not excess—it is elasticity. Discretionary spending absorbs shocks, preserves morale, and prevents burnout. Without it, even the most disciplined plan collapses under emotional strain.

The danger lies not in spending, but in unobserved spending.

Real-Time Visibility: Using a Spending Tracker to Prevent Lifestyle Creep

Identifying leaks in your discretionary third is impossible without a spending tracker that operates in real time. Delayed awareness invites rationalization. Immediate feedback invites correction. TimelyBills provides that visibility without judgment: Spending Tracker Control emerges from clarity, not restriction.

Comparative Analysis: Why the 1/3 Rule Outperforms the 50/30/20 Model in High-Inflation Cities

The 50/30/20 model assumes a stable cost structure. In cities like New York, London, or Singapore, that assumption fails quickly. Essentials alone can exceed 50% before lifestyle choices even enter the equation.

The 1/3 Rule introduces symmetry. Each category carries equal weight, forcing earlier adjustments and preventing silent erosion of savings. It is inherently more resilient in inflationary environments because it reacts proportionally rather than linearly.

Collaborative Wealth: Implementing the 1/3 Rule via a Family Budgeting Strategy

When households align, a family budgeting approach ensures everyone stays within their one-third. Shared visibility reduces conflict and replaces negotiation with structure. TimelyBills supports collective accountability without micromanagement: Family Budgeting Alignment scales stability.

Auditing Stability: Measuring What Actually Matters

Reviewing your progress through monthly reports reveals the truth about your stability—not intentions, but outcomes. Data transforms emotion into evidence. TimelyBills’ reporting tools allow households to audit proportional integrity over time: Reports Consistency compounds.

The first step toward 1/3rd mastery is to download the right ecosystem that supports proportional thinking by design, not by willpower: Download

TimelyBills brings over 10 years of experience simplifying complex financial journeys for millions across Android and iOS—experience that matters when stability is the goal.

People Also Ask

What exactly is the 1/3 rule for financial stability in 2026?

The 1/3 rule is a proportional budgeting method that allocates net income equally across essentials, savings, and discretionary spending. In 2026, its relevance comes from adaptability—it scales with income changes, inflation, and variable expenses while maintaining equilibrium. Unlike rigid models, it prioritizes sustainability over perfection.

How does the 1/3 rule differ from traditional 50/30/20 budgeting?

The 50/30/20 model underweights savings in volatile economies and assumes stable essentials. The 1/3 rule equalizes priority across survival, growth, and flexibility. This symmetry makes it more resilient in high-cost environments and better suited for modern income variability.

Can I apply the 1/3 rule if I live in a high-cost-of-living city like New York or London?

Yes, but application requires intentional trade-offs. The rule acts as a diagnostic tool—if essentials exceed one-third, it signals structural imbalance that must be addressed through housing choices, transportation adjustments, or income strategy. The rule reveals constraints rather than ignoring them.

Is it realistic to save 33% of my income with a median salary?

Realism depends on sequencing. Many households phase into the full ratio over time. Starting with proportional awareness allows gradual alignment. The power of the rule lies in directionality—moving toward balance consistently rather than achieving it instantly.

How does TimelyBills help automate the 1/3 rule for busy families?

TimelyBills automates categorization, bill payments, tracking, and reporting, reducing cognitive load. Families gain shared visibility without constant coordination, allowing the 1/3 boundaries to operate in the background while life continues.

Should taxes be included in the ‘Income’ portion of the 1/3 rule?

The rule applies best to net income after taxes. Taxes are obligations, not discretionary choices. Using net income ensures proportions reflect actual control rather than theoretical earnings.

What happens if my ‘Expenses’ third exceeds the limit?

Exceeding the limit is a signal, not a failure. It highlights structural pressures requiring adjustment—either through cost reduction, income expansion, or timeline recalibration. The rule’s value lies in making imbalance visible early.

Does the 1/3 rule account for emergency fund building?

Yes. Emergency funds are a primary function of the savings third. Once established, that portion can be reallocated toward investments or long-term goals, maintaining proportional integrity.

How often should I audit my 1/3 rule percentages using reports?

Monthly reviews are optimal for most households. This cadence balances responsiveness with stability, ensuring automation remains aligned with real-world changes without overreacting to short-term noise.

Is the 1/3 rule suitable for retirees or only for active earners?

The principle applies universally, though proportions may flex. Retirees often reframe the thirds around fixed income, healthcare, and lifestyle preservation. The structure remains valuable because it enforces clarity and sustainability across life stages.

Financial stability in 2026 is less about chasing growth and more about preserving balance. The 1/3 Rule endures because it respects human behavior, economic reality, and the quiet power of proportional discipline.

Download the app and get started on your money saving journey

© Copyrights 2026 TimelyBills. All rights reserved.